A total of 28.1 million tonnes of specialty papers will be consumed in 2025, according to the latest market report from Smithers.

Competing factors will push overall consumption to 31.3 million tonnes in 2030, equivalent to a compound annual growth rate (CAGR) of 2.1 per cent for the next five years.

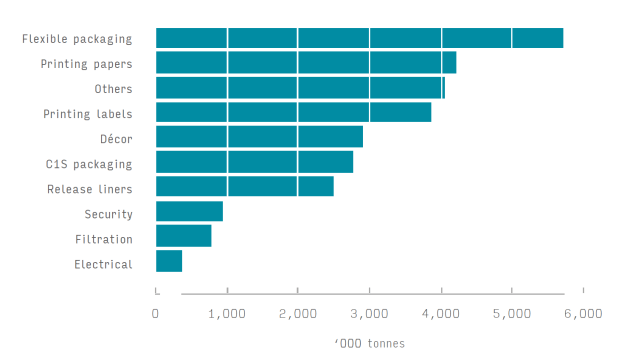

The report – The Future of Specialty Papers to 2030 – tracks consumption and technology trends across 45 separate specialty paper grades worldwide, by region and by country.

Printing papers remain an important part of the total market – although their broad outlook is depressed, strong extra sales are predicted for thermal paper, and opaque lightweight grades.

Flexible packaging papers are becoming increasingly important to the industry, with demand rising fastest for machine-glazed papers – already accounting for around half of global sales.

Sales will also be strong for coated (C1S) packaging papers over the forecast period – several machine rebuilds are set to be completed in the US, and new machines coming on stream in China.

The replacement of plastic by paper in packaging requires the development of better functional and barrier coatings, and most companies active in this space are seen to be investing in new coating chemistries, advanced substrates, and innovative ways to apply the barrier material.

In addition to the coatings, using nano-cellulose to enhance both substrates and coatings is becoming increasingly common.

Regulatory requirements are generating fresh impetus for brands to make the move from plastic to paper, but there are also challenges for specialty papermakers. New requirements, such as design-for-recyclability rules, will place extra scrutiny on how coated and metallised papers can be recovered during recycling.

As demand increases, specialty paper mills are seen to be investing in next-generation equipment.

Major chemical suppliers have introduced smart control systems to manage the addition rate on paper machines, process start-ups, and shutdowns, boosting overall efficiency. Curtain coating technology continues to advance, which is enabling multiple functional coatings to be applied from a single unit.

Asia-Pacific, China in particular, is becoming the focus for specialty paper production and new machine sales, with a forecast CAGR well above the global average.

Already accounting for 46 per cent of global output, the region’s share is seen to increase to 48.7 per cent by the end of the decade, with demand also seen to be strengthening in India.

The Future of Specialty Papers to 2030 is available to purchase now by clicking here.