The perils of putting predictions on paper - Print21 magazine feature

Forecasting the future is a hazardous task, especially in the volatile world of paper production. And, as Tony Duncan demonstrates, even the best-educated guessers can get it wildly wrong. Still, that hasn’t stopped him having a go too with some bold predictions for 2012.

December is a time for predictions, to sit back and pontificate on how the stars are going to align during the forthcoming calendar year. But before embarking on that exercise, here are some numbers and observations to provide some background (and excuses).

The current data suggest total paper consumed in Australia has dropped 4-5 per cent in the past 12 months. This is probably the lowest total tonnage consumed in recent years and continues a trend that has been seen in other developed economies.

Newsprint remains under considerable pressure, tissue may be growing slowly as an overall sector, but commercial print is losing ground and packaging is at the mercy of Australia’s primary and manufacturing sectors (i.e. packaging  follows manufacturing so as manufacturing goes offshore, then the packaging for these manufactured goods will also exit).

follows manufacturing so as manufacturing goes offshore, then the packaging for these manufactured goods will also exit).

Predicting consumption is no more difficult today than it was 10 or 20 years ago, although there is a major psychological change in that, today, the trend is obviously negative for most graphic papers in Australia (but not China, India…).

An interesting sideline issue here is that while our consumption of paper is dropping, our importance as a raw material supplier to many of these growth markets is increasing. Over the past 10 years, our exports of recovered paper fibres to primarily these markets has increased by a million tonnes, from around 350,000 tonnes per year to 1.35 million tonnes in 2011. And with an average selling price well south of $200 per tonne it is another example of flogging off a raw material for someone else to value add—and sell back to us.

Forecasts off the chart

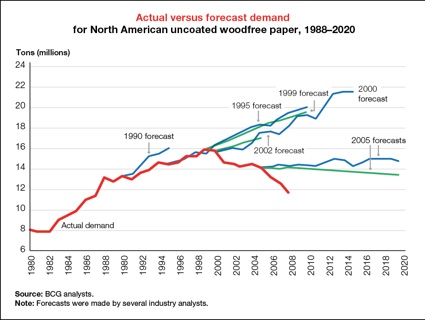

Returning to the point of predictions, the astonishing graph below from The Boston Consulting Group highlights the collective wisdom of many in the industry over the past 20 years or so. Bearing in mind that building a new paper machine is a 25+ year invest-ment, it is important that the decision-makers have an accurate view of likely demand from data supplied by credible analysts and forecasters—generally from within their companies or industry experts.

The graph below highlights a number of industry forecasts from 1990, 1995, 1999, 2000 and 2005.

The graph then plots actual demand against these industry forecasts and, as you can see, the only one which was remotely accurate was the 1995 forecast—for about 18-24 months! Absolutely no-one predicted the downturn, and even recently they have underestimated the severity of the drop-off.

Maybe the GFC has exacerbated the downturn, but as you can see from this, the negative consumption trend has been happening for many years prior to 2008.

Hindsight is a wonderful thing, and it is astonishing to think that the 2000 forecast for suggested demand now was approximately 17 million tonnes whereas the actual figure is more likely to be 11 million tonnes. The consequences have been/are considerable.

While this is based on North American market estimates, similar assumptions underpinned Australian decisions—both in manufacturing and merchanting. If nothing else it shows the power of groupthink and is probably a management case study in how senior management misread negative signs and often struggle to accept a downward trend.

The market in Australia for uncoated woodfree papers is around 430,000 tonnes of which copy paper is approximately 250,000 tonnes. However, this is probably 75,000 tonnes less than predicted by the board when the most recent uncoated woodfree paper machine was being built in Australia.

The amount of paper being sold is no longer as direct a measure of the health of the commercial print industry—the disconnect probably happened around 2003 in Australia. However it does provide some useful insights into the way the industry is travelling.

Now, let me see…

And so to some predictions:

Paper pricing: Price rises, or attempted price rises will become a regular occurrence, particularly as major merchants drive to achieve reasonable ROIs for their owners. However, what the major mill groups will do with pricing is uncertain. Most have mitigated their positions by developing manufacturing in lower cost countries which allows them to sell paper profitably outside their main regional markets. Still, there is likely to be continual pressure from their suppliers—both fibre and major chemical suppliers.

Industry: The Australian merchant industry went through the consolidation/shake-up everyone predicted. However whether this is just moving the deck chairs on the Titanic remains to be seen. With a declining market driving considerable competition, pressure on costs will remain intense as they attempt to find new market opportunities, or adjust their business downwards. Unlike printing, slicing and dicing into a range of market sectors is now almost impossible for most merchants.

Printing: The same questions will be asked in the next 12 months that were being asked 12 months ago. The industry has been going through massive transformation for the past five years, and will continue on this trajectory for 2012 without any major changes. It will be interesting to watch the amount of new large equipment being sold— and who is buying it—as this will strongly indicate which companies have solid support behind them. Industry initiatives with government will feel really good but amount to virtually nothing. The government isn’t interested.

Promotion: Sensibly the industry associations have at last got behind the global Two Sides/Print Power initiative. This does have the potential to change industry perceptions with government and customers and, if handled correctly, also has the ability to rejuvenate the local associations.

Environment: Won’t go away, and there will be some weeding out here as more complex questions are asked. There still are a number of companies using the environment as a marketing ruse but without having the fundamentals in place. The battle between PEFC and FSC will unfortunately continue to obfuscate the issues in the minds of customers. Companies should work with organisations that understand the real issues and are not focused on using it as short-term marketing fluff.

follows manufacturing so as manufacturing goes offshore, then the packaging for these manufactured goods will also exit).

follows manufacturing so as manufacturing goes offshore, then the packaging for these manufactured goods will also exit).