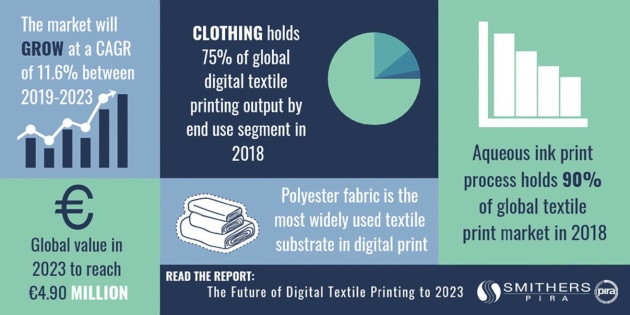

Data from a new Smithers Pira report – The Future of Digital Textile Printing to 2023 – shows that in 2018 global value in this market reached €2.83bn. This equates to 2.17 billion square metres of fabrics printed on inkjet machinery.

The good news is the market will almost double by 2023, up to €4.9bn – representative of a compound annual growth rate (CAGR) of 11.6 per cent. This contrasts to a rate of 16 per cent for the five years 2013-2017, but is symptomatic of any nascent, high-growth markets unable to sustain ultra high early growth from a low base indefinitely.

Market opportunity

Textile printing is a mature global market, but digital textile printing still forms less than five per cent of this global industry, leaving significant market share that can be targeted. Inkjet printing remains more expensive than conventional print technologies except for short production volumes.

For the print service provider (PSP), there are multiple advantages of using inkjet. These include ease of customisation, reduced cost for short production runs and much faster turnarounds. These benefits are increasingly being understood by designers, print service providers and end-users.

These capacities have been embraced most readily in the clothing and signage segments. Market trends are supporting further moves in this direction with better e-commerce sites, including direct-to-consumer platforms. More print service providers are entering textile work as ink sets, coating technology, and substrate handling improve – for example, fabric suppliers are offering more digital-ready fabric substrates, to meet burgeoning demand.

The Smithers Pira study sub-divides the digital textile market into four end-use sectors and 24 end-use applications. All will see positive double-digit annual growth by volume up to 2023.

Clothing – including swimwear, sportswear, and haute couture garments – is the largest application sector for inkjet printing, accounting for three quarters of value in the market in 2018; €2.13bn. It will maintain this position through to 2023.

Expansion in digital textile printing for home decor (household) products, such as carpets, bed linen, and curtains, will be particularly strong. This sector is benefiting from a move to embrace more freedom in interior design applications. A number of interior design companies have opened up this market with internet apps that allow amateur and professional designers to customise and mock-up their own products, such as window treatments and upholstery.

Outdoor applications

In display work on soft signage further expansion is also forecast. This will be strongest in outdoor applications as more UV-resistant ink sets become available for work such as flags and banners.

Technical textiles – which includes protective clothing, medical textiles, and automotive fabrics – is a less dynamic market and one where design innovation often plays a secondary role to performance.

This is the slowest growing digital textile end-use sector, but this is relative, with annual increases in value still forecast at nine per cent for the next five years.

Boosting productivity

Improvements in inkjet printing on textiles include innovation in both the machinery and the inks with which they are loaded.

Beginning with the printhead, a number of the latest inkjet printhead product launches and development projects involve the use of thin film piezo silicon Mems fabrication. Mems fabrication in these new piezo printheads enables a much higher nozzle density, smaller drop sizes and much higher firing frequencies, which translates to true native resolutions at 1200dpi that are capable of significantly higher print speeds.

Superior drive electronics technology is now being integrated into newer inkjet systems, simultaneously making them more scalable. The ongoing switch will continue to 2023, from custom development to standardised components using differentiated software programming developed for specific printheads and equipment applications.

Media (fabric/substrate) handling is a key part of any inkjet printing system, and one that is innovating to meet the latest demands in textile production.

Sticky belt style direct-to-fabric type handling systems are showing significant improvements in automated cleaning and better tracking eliminating major existing problems with media slippage and substrate movement.

Sticky belt style transports that incorporate the appropriate unwind and post-print collector mechanisms continue to be a good option for direct-to-fabric printing equipment with dedicated to dye-based inks for dimensionally unstable fabric applications. Other roll-to-roll wide and super-wide format printer models are successfully using a trough style ink capture solution that is acceptable for some direct- to-fabric applications.

Newer inkjet printer designs are factoring in more print production process requirements. Some are jetting primers – or optimisers – on the substrate only in those areas to be printed, which then need to be dried with heat and air prior to applying the ink. More air and heat is then applied after the colours to enable spot or flood coating and then more heat and air to provide final drying and fixing. Within this added complexity, the overriding rule is that the faster the system, the more sophisticated the drying/heating/curing requirements become.

Hybrid direct/sublimation aqueous dispersed dye ink is becoming more popular as higher speed wide-format and grand-format roll-to roll-inkjet textile systems enter commercial print production. With reference to substrate handling, many of these systems offer the ability to switch back and forth from paper transfer to direct-to-fabric (DTF).

Some consumable suppliers have introduced pre-treatment fluids that help manage the appropriate amount of bleed for two-sided fabric applications, such as flags. These typically higher colourant content ink sets are also benefitting another sub-segment of textile digital printing – display graphics, both frontlit and backlit.

While reactive dye inks still provide excellent colour gamut and performance on natural fabrics such as cotton, aqueous pigment inks are reaching similar colour and performance while being much simpler and environmentally friendly in terms of post-print production.

Cross fertilise

Development in formulations for these types of inks for other print applications is likely to cross-fertilise the digital textile segment, especially around the interaction of inkjet inks with synthetic substrates and coatings. These aqueous pigmented inks are increasingly formulated for high-speed roll-to-roll production on a wide variety of fabrics.

The impact of key end-user and technology factors on future expansion of digital textile printing is examined in detail and quantified in the newly available Smithers Pira study The Future of Digital Textile Printing to 2023.